Let’s dive into the DSCR Loan Texas Guide 2024. You can find many guides on the internet, but this guide differs from others.

It will help to understand DSCR loans in Texas in a better manner.

We will cover the DSCR loan Texas in brief.DSCR loans in Texas, explaining what they are, how they work, and why they matter for real estate investors. What are the pros and cons of a DSCR loan and more?

Also Read: What is 1 Infinite Loop CA Charge on a Credit Card

Inside the Article

What is a DSCR Loan?

If you’re considering real estate investments in Texas, you might have heard the term “DSCR Loan.” DSCR, which stands for Debt Service Coverage Ratio, is crucial in commercial real estate financing.

A DSCR loan is also known as a Debt Service Coverage Ratio loan. It is a type of commercial real estate financing that focuses on the property’s ability to generate enough income to cover its debt obligations.

In other words, lenders check whether the property’s rental income can support the mortgage payments and other related expenses.

How Does DSCR Work?

The Debt Service Coverage Ratio is calculated by dividing the property’s net operating income (NOI) by its total debt service (mortgage payments plus other related costs). The formula for DSCR is:

DSCR = Net Operating Income / Total Debt Service

Net Operating Income (NOI): This is the income generated by the property after deducting operating expenses like property taxes, insurance, utilities, and maintenance costs.

Total Debt Service: This includes the principal and interest payments on the mortgage as well as any other related costs, like property management fees.

In general, lenders look for a DSCR of at least 1.25 to 1.30. This means that the property’s income is 1.25 to 1.30 times greater than its debt obligations. A higher DSCR ratio indicates a stronger ability of the property to cover its debts and is generally more favorable to lenders.

Let us understand with a Simple example.

Suppose, your yearly rental income is $20,000, and your total yearly expenses, including mortgage and other costs, amount to $15,000.

In this case, your DSCR is 1.33.

This means that your income is 1.33 times more than your expenses. which is a good sign. It shows that you have a comfortable shield to cover your costs. you may qualify for favorable loan terms.

Now, let’s say your annual rental income is $10,000, and your yearly expenses reach $12,000.

This would give you a DSCR of 0.83. When the DSCR is 1, your income matches your expenses.

When it’s less than 1, like in this case, it indicates your income isn’t enough to cover all your costs. Lenders might find this riskier, making it potentially harder to secure a loan.

Read Also: Ledger Green Credit Card Charge

Why DSCR Matters for Real Estate Investors in Texas?

DSCR is a crucial factor for both lenders and investors in the Texas real estate market. Here’s why:

- Lender Assessment: Lenders use the DSCR ratio to assess the risk of providing financing for a commercial property. A higher DSCR indicates a lower risk, as the property’s income is covering its debt payments.

- Loan Approval: For investors, having a strong DSCR increases the chances of loan approval. Lenders want assurance that the property can generate enough income to repay the loan.

- Property Viability: DSCR also helps investors check the viability of a potential investment. If the property’s DSCR is below the desired threshold, it might indicate that the rental income is insufficient to support the investment.

- Cash Flow: A healthy DSCR ensures positive cash flow for investors. It indicates that after paying all expenses, there’s still enough income left over to cover the debt service and generate a profit.

Eligibility for a DSCR Loan

We already delved into the concept of a DSCR loan, understanding how it operates and how to calculate.

At this point, you might be wondering who can apply for this loan and whether you qualify. Generally, to be eligible for a DSCR loan, certain criteria need to be met:

- Investment Property: DSCR loans are for properties you want to invest in, not for your own home.

- Strong Income Potential: Your property should be able to generate enough rental income to cover the loan payments.

- Good Credit Score: Having a solid credit score makes it easier to get approved for a DSCR loan.

- Down Payment: You’ll need enough money for a down payment on the property you’re investing in.

- Positive Cash Flow: The property should make more money than it costs to run, so it can cover the loan payments.

- Understand DSCR: Knowing how the Debt Service Coverage Ratio works is important, as lenders use it to assess your loan application.

- Prove Your Experience: Some lenders might want to see that you have experience in real estate investing.

Remember, the specific requirements can vary between lenders and situations, so it’s a good idea to talk to professionals to see if you meet the criteria.

How to apply for a DSCR Loan?

In Texas, the DSCR loan concept applies to other regions. However, the local real estate market conditions, property values, and rental income potential will influence the specific DSCR ratios that lenders expect.

It’s essential to conduct thorough research on the Texas real estate market and work with local professionals to ensure you’re making informed decisions.

Let us understand how to apply for a DSCR loan.

- Find Lenders: Look for the Best financial companies that offer DSCR loans.

- Select Lender: Select the best lender that meets your requirements.

- Gather Documents: Prepare documents like your rental property details, income statements, and expenses. These help show how much money the property makes and spends.

- Contact Lenders: Get in touch with the lenders you found. You can call, visit their office, or even apply online through their website.

- Share your Plan: Talk to the lender about your investment plan and the property details. They’ll help you understand if a DSCR loan is a good fit.

- Fill Application: The lender will give you an application form. Fill in your personal and property details accurately.

- Provide Documents: Attach the documents you gathered earlier. These help the lender assess your financial situation and the property’s potential.

- Wait for Approval: The lender will review your application and documents. This might take a bit of time. They might ask for more info if needed.

- Receive Offer: If the lender approves your application, they’ll make you a loan offer. This includes details about the loan amount, interest rates, and repayment terms.

- Accept the Offer: If you’re okay with the offer, you can accept it. Read through all the terms carefully before agreeing.

- Receive Funds: After you agree, the lender will finalize things and give you the loan funds. Now you can use the money for your investment property.

Remember, each lender might have slightly different steps, so it’s good to follow their instructions closely. Also, if you’re unsure about anything, don’t hesitate to ask questions with your lender.

What is Meta PPGF Charge on Credit Card?

Best Companies For DSCR Loan in Texas

Here we are listing the best Companies that offer DSCR loans in Texas.

- Griffin Funding

- Angel Oak

- JMAC Lending

- Tuss Financial Group

- Corevest

- Texas Hard Money

DSCR loans in Texas, a range of reputable companies offer exceptional services specialized to investors’ needs.

Griffin Funding is renowned for its flexible DSCR loan options. This company is also known for the availability of interest-only repayment plans.

Texas Hard Money Pros specializes in hard money loans, providing personalized solutions to meet diverse investment requirements.

CoreVest Finance boasts a strong track record in real estate financing. It offers a diverse selection of loan products to suit various investment strategies.

Angel Oak and JMAC Lending offer innovative lending solutions, while Tuss Financial Group provides a comprehensive approach to real estate financing.

All these companies have consistently demonstrated their commitment to helping investors achieve their real estate goals through well-structured DSCR loan options and exceptional customer service.

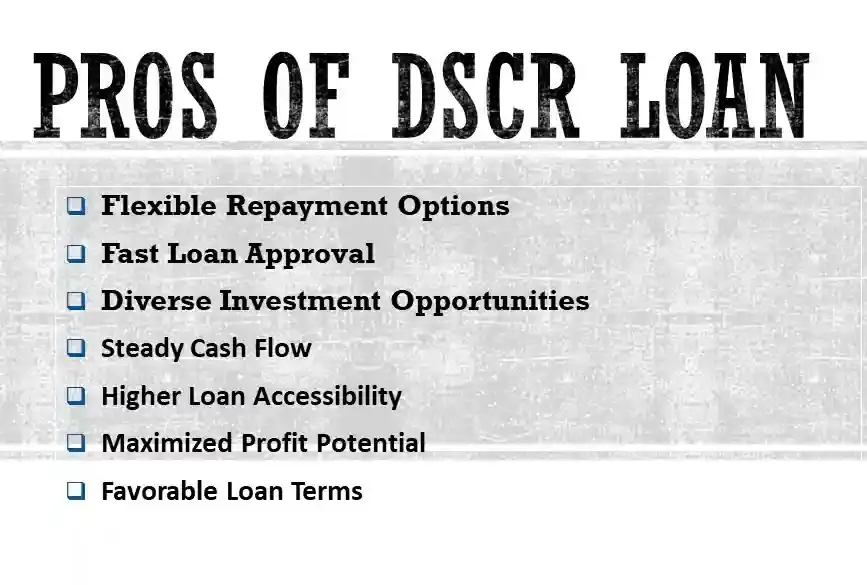

Pros of DSCR Loan

Let us understand what are the benefits of a DSCR loan.DSCR loans are awesome for real estate investors.

These loans are flexible, meaning they’re easier and faster to get. You can start by paying just the interest, saving money at first. If you want a smart loan for your investment, DSCR loans can be a great choice.

- Diverse Investment Opportunities: DSCR loans can be utilized across multiple properties, allowing investors to diversify their investment strategy. Options include focusing on multiple properties in a single Texas city or distributing investments among the state’s major cities.

- Swift Approval Process: DSCR loan approval doesn’t rely on traditional income verification methods like W2 forms. Consequently, these loans are typically approved within weeks, making them an excellent choice for investors seeking swift entry into the Texas market.

- Flexible Repayment Options: Premier lenders offer various repayment choices for DSCR loans, including adjustable-rate, fixed-rate, and interest-only mortgages. This flexibility empowers borrowers to select the repayment method that best suits their financial circumstances.

- Nationwide Exploration: For those interested in exploring hard money loans beyond Texas, a national overview of DSCR loans is a valuable starting point. It can provide insights into potential opportunities in other states.

Cons of DSCR Loan

Every loan comes with its benefits and drawbacks. While taking a loan you should consider both aspects of the loan. We already shared what are the benefits of a DSCR loan. Let’s understand what are the drawbacks of the DSCR loan.

- Limited for Investors: DSCR loans are mainly for people investing in properties, not for buying homes to live in.

- Not for Quick Money: If you need money fast, these loans might not be the best option since they’re tied to properties and take time.

- More Interest Over Time: Starting with just interest payments can save money early on, but you might pay more overall in the long run.

- Not Easy for Everyone: DSCR loans might not work if you don’t have a strong credit score or enough money for a down payment.

- Focused on Cash Flow: These loans care a lot about how much money the property makes, so if it doesn’t earn much, you might struggle.

- Complex for Newbies: Understanding DSCR ratios and calculations can be confusing, especially if you’re new to investing.

- Risk of Losing Property: If the property doesn’t make enough money to cover the loan, you might lose the property to the lender.

The Conclusion Point

We have explained the DSCR Loan in detail hoping that now you understand this loan.

These loans provide a way for lenders and investors to assess the property’s financial health and its ability to generate income to cover its debts.

FAQs on DSCR Loan

What is a DSCR loan?

A DSCR loan is a type of loan for buying investment properties. It looks at how much money the property can make compared to the loan payments.

Who can get a DSCR loan?

Investors who want to buy properties to rent out can apply for DSCR loans. These loans are not for people buying homes to live in.

How is DSCR calculated?

DSCR is found by dividing the property’s income by its expenses. It shows if the property makes enough money to cover the loan payments.

What is the DSCR loan Texas interest rate?

The interest rate of a DSCR loan, Current DSCR rates average between 7.65% and 8.65%. It can vary with time.

Can DSCR be negative?

Yes, it can be negative which means negative cash flow. The borrower may not pay debt obligations without extra borrowing outsourcing.

What is the maximum loan value?

Maximum loan value depends on various factors. It can be different for every real estate investor. A lender’s willingness to lend you money when you apply for a secured loan is subject to a maximum loan-to-value ratio. It describes the sum of money they are prepared to lend about the price of the asset serving as the loan guarantee.